GomSpace (GOMX)

GomSpace (GOMX)

It’s Easter and thus this third edition of ValueTeddy’s Snap Judgements is slightly delayed. I hope you have had a nice holiday, and that you find this letter interesting.

GomSpace

Ticker: GOM

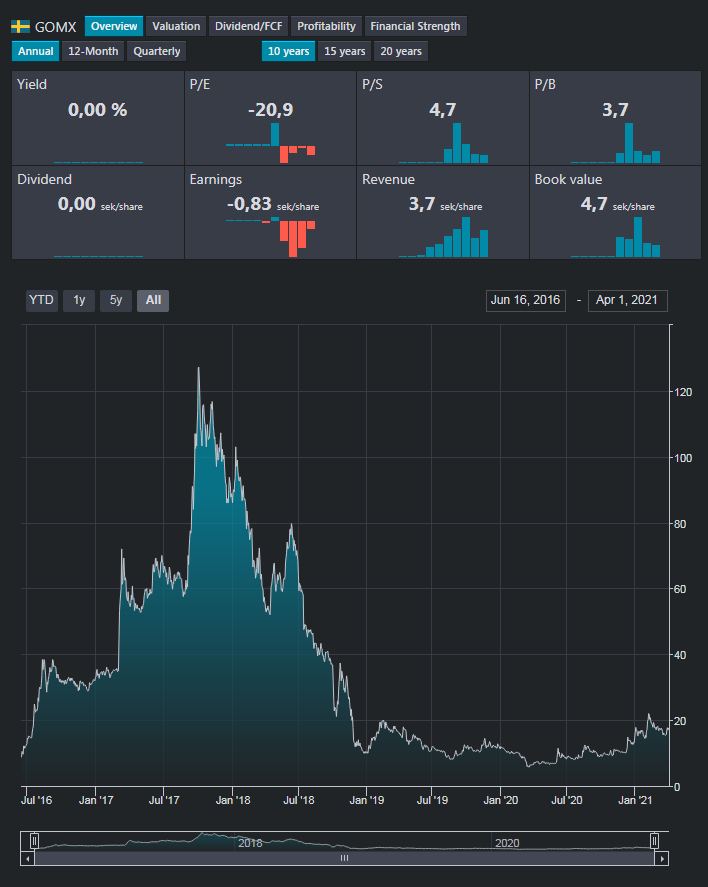

Market cap: 911 m SEK

Revenue: 194 m SEK

I remember a few years ago where space and micro-satellites was the big thing on Swedish FinTwit. GomSpace is one of those very hot stocks at that time, and it has seemingly come back to earth since.

First of all, this is a Denmark based company, but its listed in Sweden. It’s not dual listed in DK as well but its only listed in Sweden. This always raises an eyebrow, and I generally feel suspicious of companies listed in countries other than where their HQ is. Of course there might be cases where this makes sense, but I always feel it should be examined.

GomSpace is provide parts and subsystems for small satellites, as well as whole satellites and control software etc. This is not an entirely uninteresting sector, and it’s one where I think I could get a feel for the business and its competitors.

Financials

Moving to the finances from the full year as reported in the Q4 for 2020, we see a significant increase in revenues and gross profit. Revenues grew 42% from 136 m to 194 m and gross profit grew ~160% from 18 m to 47.6 m. However they are till making an operating loss of 30 m, which is an improvement compared to last years loss of 113 m. Looking at the operating costs, I note something interesting. Nearly every line item has decreased. This causes me to suspect something tricky regarding the sales cycle in this industry, but I might be wrong. In my experience it is challenging to increase revenues while at the same time decreasing SG&A costs. This should be something to look into before investing in this stock, since the decreased SG&A could be foreshadowing an upcoming decrease in sales.

So this is a company I would pass on simply since it is not operationally profitable. As far as I can tell, GomSpace need to double gross profit while not increasing overhead by anything in order to reach operating profitability. For the sake of the letter we are still moving on to the balance sheet and the cash flows, even though this is where I would pass.

GomSpace carries 102 m in short term debt and 53 m in long term debt, against 247 m of equity. On the asset side they have 65 m of pp&e and 214 m of current assets (of which 135 m is cash). The debt seems to be well matched against the assets. In other words there are short term assets to match the short term debt, and the long term debt seem to have funded long term assets.

Moving to the cash flows we see a net positive cash flow from operations of 43 m compared to a cash burn of 92 m the year before. When a company is like this, it is really important to look at what adjustments cause the operating loss to still provide positive operating cash flow. In this case, the largest adjustments are 1. depreciation and amortisation, 2. change in working capital, and 3. changes in financial items and tax received. If this were a deeper analysis, this is a point where I would put significant time and effort, especially in this case where the operating profits are negative and the operating cash flow is positive.

The D&A change is about same as last year nothing odd here, and the change in financial items and tax is roughly same as last year also. Being a net receiver of tax is not something one should rely on, and if the company turns profitable this is something that will change. Also, reversing financial items only makes sense when looking purely at operations, it is a very real cost. That leaves the changes in working capital, in this statement labelled as change in inventories, trade receivables, other receivables, and change in trade and other payables. It is normal for these line items to fluctuate, but in GomSpaces case the final line (trade and other payables) is a net cash contribution of 33 m, compared to a net cash deduction of 49 m last year. This is something we also can see in the balance sheet as a decrease of receivables and an increase in payables. This causes me to think that the net positive cash flow from operations might be temporary, and it is something one should take a close look at in this case.

Valuation

With all that said, let’s look at the valuation. GomSpace trades at about 250 times EV/EBITDA and a P/S of 4.7. Maybe I’m missing something here, but it looks to me like there is a lot priced in here. There are two big questions in these sorts of cases, 1. when will they be profitable, and 2. how much capital needs to be raised before that happens. In this short and brief analysis I have way too little information to answer either question, but to me it looks to be far out. However, they have cash on hand so they wont need cash immediately, and if they can keep operational cash flow positive it not impossible for them to reach real operational profitability. This does not look like a screaming buy to me, but it’s nonetheless an interesting case.

Parting words

I hope you liked this edition of ValueTeddy’s Snap Judgements! If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com. Please note that this is in no way a recommendation or financial advice and I’m not your financial adviser.