Embracer (EMBRAC)

For this edition of ValueTeddy’s Write-ups, we are taking a look at the very impressive workings of Lars Wingefors. It is of course Embracer, which in just a few years has acquired its way to a multi-billion SEK market cap. Since its IPO at 9 SEK in November of 2016, it has returned about 2400%, or about a 120% CAGR.

What is it?

Embracer (Formerly THQ Nordic) is a group divided into what they call 8 operating segments, totalling 77 game development studios. This is roughly how each operating segment compares in terms of the last four quarters revenues (note that Easybrain and Gearbox were merged with during the quarter, and note that CrazyLabs were acquired after the end of the quarter):

Koch Media/Koch Film, 2.5 bn sek

Deep Silver, 2 bn sek

Easybrain, about 1.9 bn sek (full year 2020)

THQ Nordic, 1.8 bn sek

DECA Games/CrazyLabs, 1.5 bn sek

Gearbox, 1 bn sek (9 months)

Saber Interactive, 1.1 bn sek

Coffee Stain, 1.1 bn sek

Some readers might have noted that my list is not identical to the graphic they post on the corporate website, and this is because this is how they report their segments in the reports. For some reason, they lump Koch Media and Deep Silver together when presenting their operating segments, while presenting Amplifier as a separate operating segment. However, in the reports, they report Koch Media and Koch Films as one segment, and Deep Silver as another, and Amplifer is reported in the THQ Nordic operating segment. I don’t really know why they do it differently between the website and the financial reports, but this is how they currently present it. Without further ado, lets briefly present each segment.

Koch Media / Koch Film

This segment is the partner publishing arm of Embracer, and it is one of the leading global third party publishers. Koch is headquartered in Munich, and works within physical and digital publishing of games, merchandise, and films in the US and Europe. There is also a quality assurance outsourcing company called Quantic Lab within this segment.

Deep Silver

Deep Silver is honestly quite strangely integrated into Embracer, since it is formally under Koch Media. Deep Silver is headquartered in Munich, and contains 10 studios and four publishers. They are mainly focused on large PC and Console titles, and some of their more famous IPs are probably Metro, Dead Island, and Saints Row.

Easybrain

Easybrain was merged with during the quarter, and it was established as a separate operating segment. It is a leading mobile developer headquartered in Cyprus, focused on free-to-play puzzle and logic based games. Some of their most popular titles are Sudoku.com, Nonogram.com, and Killer sudoku.

THQ Nordic

THQ Nordic, headquartered in Vienna, holds 16 studios and two publishers. They focus on developing and publishing games for PC, Mobile, and Console. They have developed and published games such as Biomutant, Darksiders, the Guild, Vermintide, Ori and the Blind Forest, and Desperados 3.

DECA Games/Crazy Labs

DECA recently merged with Crazy Labs after the end of the quarter, so the following information may change as of the next report. Currently, DECA is headquartered in Berlin, and house five studios/publishers. DECA is focused on acquiring established game IP, assets, and licences, and then “applying operating expertise to grow audiences and improving profitability”, and is mainly focused on the Mobile market.

Crazy Labs is a “top 3 mobile games publisher and developer according to AppAnnie and Sensor Tower” focused on casual and “hyper-casual” mobile games, headquartered in Tel Aviv.

Gearbox

Gearbox was acquired during the quarter, and is a developer and publisher of games, mainly aimed at the PC and Console markets. They are probably most famous for their widely popular Borderlands franchise, but they also developed the Brothers in Arms franchise, Duke Nukem, the original Counter-Strike game, and the classic Tony Hawks Pro Skater 3.

Saber Interactive

Saber is an independent developer and publisher of PC, Console, and Mobile games, headquartered in Fort Lauderdale. Within the segment is 14 studios and one publisher. Some of their recent releases have been adaptations of The Witcher 3 to the Switch and the the latest Xbox and Play Station consoles, World War Z, Snowrunner, Crysis Remastered, and Halo Master Chief Collection.

Coffee Stain

Coffee Stain houses four studios, two “associated studios”, and one one publisher. It is headquartered in Skövde, and have developed and published games popular such as Satisfactory, Goat Simulator, and Valheim.

Short History

Normally, I don’t go over the company history, but Embracer has a quite short history, and I’ll tell an extremely shortened version. In the 90’s and early 00’s a then teenage Lars Wingefors does some mail order business and later buys a videogame wholesaler, named Game Outlet Europe (today a part of the Koch Media segment). GOE starts a publisher called Nordic Games in 2007, and buys the insolvent publisher JoWood in 2011. In 2013 Nordic Games buys a bunch of IPs from THQ inc, in 2014 the two parties merge forming THQ Nordic, and they go public in 2016. In 2018 they make a huge batch of large transformative acquisitions and mergers, acquiring or merging with Koch Media/Deep Silver, Coffee Stain, Voliotion, Bugbear, Handygames, and Lavapotion. In 2019 they change name from THQ Nordic to Embracer, to avoid confusion between the subsidiary and the parent company. In the three years between 2016 and 2019 sales exploded from just north of 300 m SEK to over 5 billion SEK, and the headcount grew from less than four hundred to over three thousand. Between 2019 to today, Embracer has made over 20 acquisitions, the largest being Gearbox, and Easybrain in 2021, but also Saber Interactive in 2020. As I am writing this, Embracers total sales should be in the ballpark of over 12 billion SEK and the total headcount exceeds 6000 people.

Valuation Approach

So lets pause for a second and think about what we are looking at here. The current group has 77 studios and over 240 IPs under their umbrella. Many of the segments do both development and publishing of both internal and external games. So how do we look at it? I argue that the current division into eight segments fill very little purpose for us as external investors when trying to understand Embracer and their business. Instead, I think we do best in looking at Embracer as one single unit. Furthermore, as you might be able to tell from the short history part, Embracer really likes acquisitions, which makes the future incredibly hard to predict. This also makes it difficult to compare the current financials to the historic financials. With that said we will move on to some numbers.

Financials

As of writing, the Q4 for the fiscal year 2020 (ended in March 2021) is the latest report, and I will be adjusting the figures to what I believe will account for all the acquisitions not yet consolidated into the reporting. As far as I can tell, the acquisitions not yet in the reported numbers are Gearbox, Easybrain, Aspyr, and CrazyLabs. Figures will be in SEK. Here’s what I’m using and where I’m getting the figures from (everything can be found on Embracers IR website):

Embracer - Full fiscal 2020, from the Q4 2020

Gearbox - First 9 months 2020, from the merger announcement plus 10%

Easybrain, Aspyr, CrazyLabs - Full year 2020, from the merger announcement

Here are the figures I have come up with (figures in million SEK):

In aggregate, I end up with the following approximated financials: 13.6 billion SEK in revenues, 1.7 billion SEK in operating income, and 5.4 billion in operating cash flow. Regarding the balance sheet, at the current market cap of about 89 billion SEK, I get an enterprise value of about 76 billion SEK. This uses the last quarterly balance sheet, and is not adjusted for the latest acquisitions.

There are no detailed numbers out for Gearbox, Easybrain, Aspyr, and Crazylabs, so here’s how I got to my figures. The revenues and operating income are given in the materials listed above, except for CrazyLabs which only gives revenue. For CrazyLabs I assume a 10% operating income margin, and for Gearbox I am using the 9-months figures and adding 10%, which I think is very conservative.

The operating cash flow for Embracer is taken from the latest report, and for Gearbox, Easybrain, Aspyr, and Crazylabs I assume a 30% operating cash flow margin, which is lower than Embracers 44% operating cash flow margin.

The Troubles

Here are the troubles: Embracers acquisitions cause the depreciation and amortisation to be pretty close to whatever they want. This is a topic that you could pour hours and hours into, but I will try and keep it as brief as possible. The gist of it is, when a game company develops a game, the work is either expensed or capitalized on the balance sheet. If it is capitalized, it’s then written off as the game is released and starts generating revenue. The problem arises when this development was done in a company, which is then acquired by Embracer. Embracer will now get revenue streams, but not have the capitalized work to depreciate. The solution to this is whats called PPA (Purchase Price Allotment) and the idea is to allocate the appropriate amounts of the purchase price between Capitalized game development, Intellectual Property rights (IP) and Goodwill. The key here is that the depreciation on either Goodwill nor IP decrease the “operational EBIT” that Embracer is reporting, because these are deemed “acquisition related depreciation”.

Furthermore, the depreciation schedule is different for capitalized game development, IP-rights, and Goodwill. Where development is written off over two years, whereas IP and Goodwill are written off over 5 years. This is how the PPA materially affects the earnings for the coming years. More allotment to IP and Goodwill gives higher earnings for the next two years, compared to a higher allotment to capitalized development which gives lower earnings in the near term but higher earnings past the two year depreciation.

This matters because it results in pretty tricky accounting, and it is kind of difficult to figure out what the actual operating income, earnings, and the actual free cash flow is. Because of this, I will use my estimate of operating cash flow in valuation, but I have no idea what the capital expenditures will be 2021, or any year going forward. One method is to go off the investments, and just assume all of it is CAPEX. I am not going to do that, and instead use the figures in the end of the quarterly report regarding their investments in intangible assets. The table will be in the appendix, and there they do separate the different depreciation and amortisation line by line, but as this section is trying to explain is that these figures are very difficult for us to validate. And this matters because of the classification of operating and acquisition related depreciation.

Valuation

because of “The Troubles”, I think the best way for me to value Embracer is on an operating cash flow basis.

Looking at the market cap of 89 billion and the EV of about 76 billion, we get an EV/OPCF of about 14 and the P/OPCF is about 17 on my estimated 2021 figures.

Some Good Stuff

First of all, consider the largest owners:

It is abundantly clear that Lars Wingefors, Co-Founder and CEO has a huge amount of skin in the game, with almost 30% of the capital. The second largest owner in the list is connected to Saber, and many of the managers have shares to varying degrees. I would be more on the fence regarding this kind of very acquisition heavy business if Lars did not have so much of his own money on the line.

Furthermore, the organisational structure, even though I expressed some confusion regarding the reporting segments, the operational rationale behind the segments make a lot of sense. Here I thank a bunch of people on Twitter for great discussions which helped me understand this. The organisation is very decentralized, and the studios all remain independent and in control of their own development projects etc. The upside is that they also act as sources for potential M&A targets, but the deals have to be approved by headquarters. So I think they are getting both the benefits of a decentralized structure of independent studios, but they still also capture some of the benefits that come with scale. Embracer also want to have a long term mindset in their purchases. They appear not to just purchase studios, strip them of all their developers, and then leaving them to die, but instead they want to enable them, and let them develop their IPs. I think this is a very important advantage, to have the appearance of an attractive home for the acquisition target.

Discussion

The returns we can expect given this multiple rests on three factors: growth rate of OPCF, future P/OPCF multiple, and future share dilution. These three are all hard to estimate, and I have no clear answer for any of them. But lets look at the near term history.

For the full year, the revenue grew sales by 72%, and they more than doubled their operating cash flow. From 2018 until today, the sales have grown by almost 200%, and the operating cash flow has grown almost 1000%. During the same period the share count increased by about 70%. So looking backwards, Embracer have grown at an insane pace, and they have been issuing a fair amount of shares to do so.

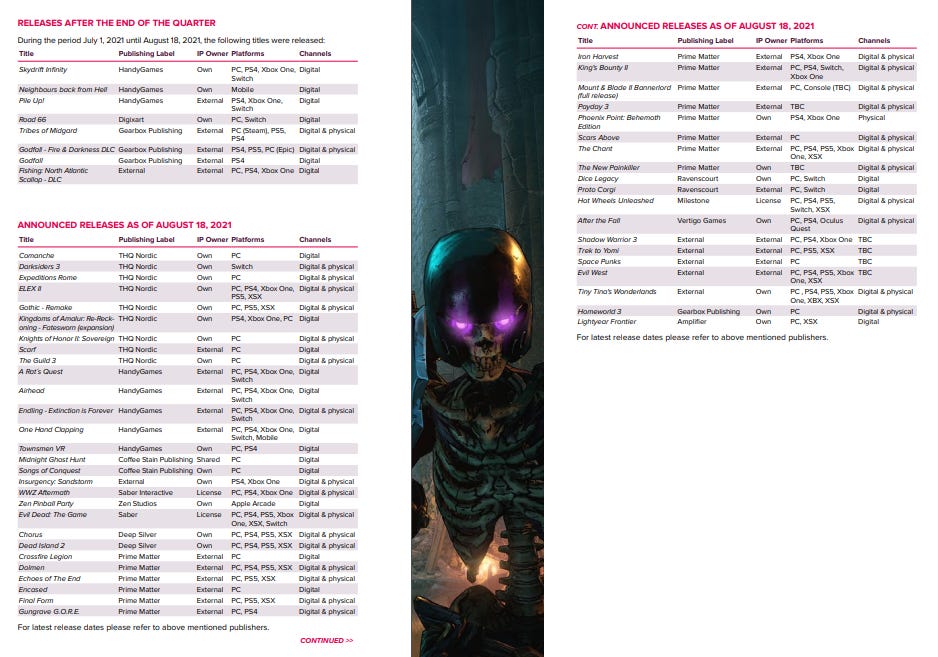

Going forward, I think Embracer can keep pushing for growth. Maybe not at the same pace as historically, but still growth. If Embracer does not find acquisitions, at least the share count doesn’t increase, and all the studios they already own have a considerable pipeline and backlog of games. In the appendix there will be a summary of the announced releases.

Considering the possibility for continued growth, high margins, a founder with lots of shares, and the advantageous organisation structure leads me to like the bet around the current price. The valuation is, in my opinion, low enough that even if growth rate is not as extreme as before, there should be a very low risk of multiples contracting. If there isn’t a spree of acquisitions, there is a large catalogue of games, and some releases to look forward to.

Normally I would have liked to have some estimated target return, but It’s tricky in Embracers case. If they make a lot of acquisitions, they will issue more shares, but the net result should be positive. The acquisitions can boost the growth numbers, but the share issues also dilute the current shareholders. If they don’t acquire a lot of companies, the growth rate will be lower, but they won’t need to issue shares.

My conclusion is that I like the potential returns of Embracer around the current price. The nature of the company makes it incredibly hard to predict what kind of returns I am looking at here, but I think the risk-reward is better in Embracer compared many other opportunities out there. So somehow I end up liking the stock, but I don't have any clue what my expected return would be here, which makes me somewhat uncomfortable.

Some Risks

The largest potential risk is that the balance sheet has overstated Goodwill and IP, which would cause very large write downs. Going forward, one other risk is that if the quality of the future acquisitions or mergers are of lower quality, and if Embracer overpays for them using shares this will have a very negative effect on the value of the business. In these cases, there is also the risk that key people in the acquired business decide to leave after a while, which of course would be unfortunate. Finally, Lars Wingefors is a very important part of the puzzle currently, so if he should for some reason decide to retire or sell his shares for whatever reason, then I assume the share price will take a dive.

Parting words

I do not own any shares in Embracer as I am writing this, but I will look to purchase shares, and might own shares when you are reading this. This is not a recommendation to buy or sell anything, nor is it financial advice. Always do your own research.

Note that the report for the first quarter of 2021 will be released on the 18.08.2021, and I will update the table and the list of the announced releases in the appendix when the report is published.

I hope you liked this edition of ValueTeddy’s Write-ups! I had some really interesting discussions on Twitter about Embracer, so huge thanks to everyone that discussed Embracer with me! If you want to suggest stocks for me to look at, you can tweet @ValueTeddy, and do check out valueteddy.com. Please note that this is in no way a recommendation or financial advice and I’m not your financial adviser.

Appendix

Parts of the Summary table of some KPIs (from page 40 in the Q1 report 2021)

(This was updated on 18.8)

@financeamir’s tweet regarding PPA (use google translate)

The current pipeline of announced game releases:

(This has been updated as of 18.8 from the Q1 21 report)

Excellent post. A bit late to read it but it's still very relevant today. I am very excited about the group but arrived at the same conclusion as you, namely that because of all the noise with acquisition costs and how they are amortized or not, I am unable to properly value the business. You'd really have to do sum-of-parts valuation to get comfortable. Still, I am comfortable enough with the general directionality of the business to take a small position that I would grow over time if I see the performance improving.

Helpful. Thank you!